This week, Shimano announced its third-quarter financial results, in which it revealed a 12 per cent drop in sales of its bicycle components when compared to the same period – the first nine months – in 2023.

The report, which shows sales down to 253.8 billion yen (£1.28 billion) and income down by 26 per cent to 41.3 billion yen (£207 million), looks to cut a negative picture at first glance, but Shimano’s analysis of the situation is one of optimism.

It cited the ongoing war in Ukraine and tensions in the Middle East as reasons for “downward pressure on the economic climate,” but suggested that global economy was showing “signs of a pickup” as a result of subsidised high inflation. It added that in Europe, the economy was “starting to show signs of recovery,” but that the “pace of economic expansion was moderate” in the USA.

Analysing the long-term trends, Shimano’s business looks to still be stabilising following the peak it experienced as a result of the pandemic.

Shimano has two main sectors of its business. The bicycle sector makes up approximately 75% of sales, while fishing tackle makes up the bulk of the remaining 25%.

Analsying the years

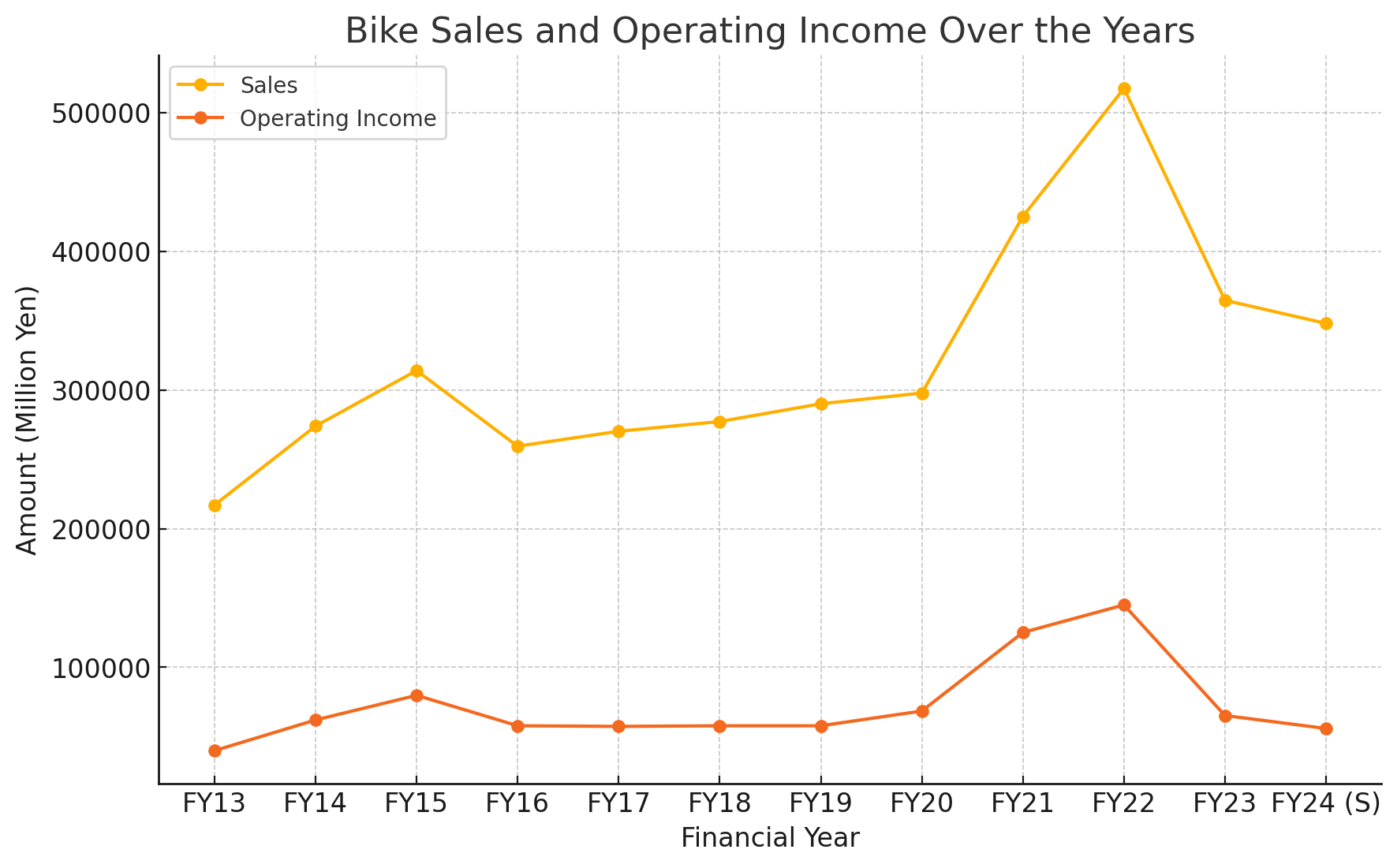

In the bike industry alone, if we normalise for the pandemic-led anomalous years, the company’s sales have been on a moderate upward trend since 2013, as the below graph shows.

For the FY24 data, Shimano has used the first nine months of the year and projected a year-end revenue forecast. (Image credit: Future)

Overlaying the operating income – essentially the brand’s profit – to that same graph, we can see that it has remained steady.

The latest race content, interviews, features, reviews and expert buying guides, direct to your inbox!

Between FY16 and FY19, profit sat at 57 billion yen for four years, despite sales growing from 259 billion yen to 290 billion yen in the same period.

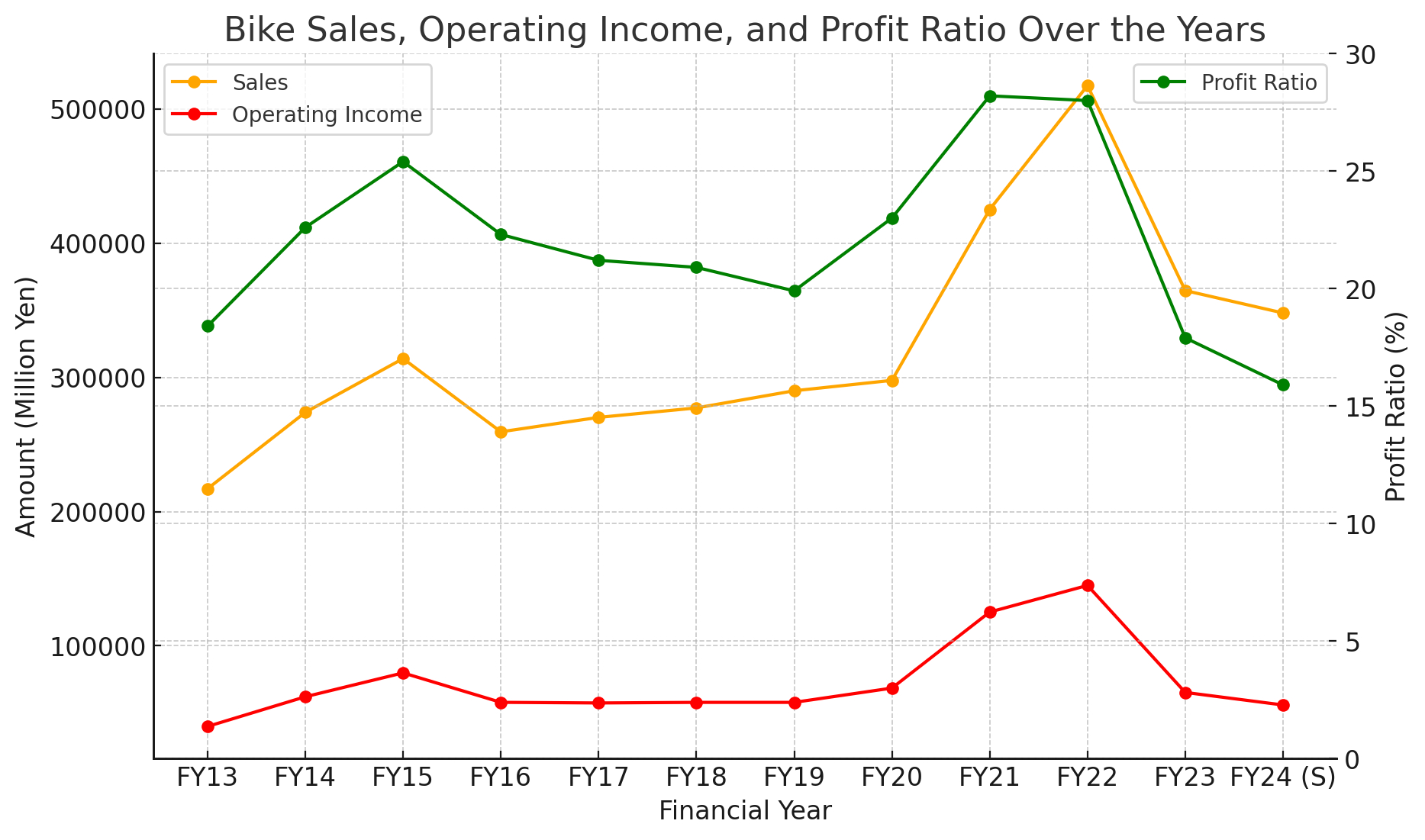

Next, we’ve overlaid the profit margin, as shown below.

With forecast sales of 348 billion yen and a forecast operating income of 55.5 billion yen. Shimano’s predicted profit margin for FY24 is its lowest in a decade. The company’s operating income from the bike sector is in line with the growth it was seeing before the pandemic, and the profit margin looks to follow the pre-pandemic trajectory too.

Given the outsized impact of the pandemic, it’s hard to know whether the data from 2023 and 2024 are reliable indicators of future performance, or whether the industry – and in turn Shimano – will continue to peak and trough in the coming years.

It’s also important to remember that in September 2023, Shimano announced the recall of over a million Ultegra and Dura-Ace cranksets, a recall it later claimed was costing $18 million to foot the bill.

We’re yet to see that data listed in the FY24 accounts though. In year-end results for FY22 and FY23, ‘Voluntary Recalls’ is listed as a line under Non-Operating Expenses, and is quoted at 1 million yen ($6,500) for FY22 and 1.4 billion yen (9,000,000 USD) for FY23.

However, Voluntary Recall doesn’t feature in this Q3 report. There is 1.9 billion yen simply listed under ‘Other’, but presumably we’ll have to wait for the year-end results to see the latest cost of that.

In May, Shimano launched a 12-speed version of its GRX gravel groupset, and elsewhere in the report, Shimano makes a point of highlighting this. It says the Group “received a favorable reception for its products,” where it also called out the 2023 launch of the road-going 105 groupset.

Why is this important?

Given the scale of Shimano and its prevalence on bikes all the way from the grass-roots to the high-end, the Japanese brand is seen as something of a bellwether for the health of the wider bicycle industry. Its performance in different geographical markets also provides a worldwide picture of the industry’s global state.

For example, the report shows that forecasted total sales in Europe will match pre-pandemic levels in FY24, while the market in China will exceed even the pandemic peak, and is set to finish more than double the 2019 total.

Also interesting is that sales to North America only make up approximately 6% of the total sales volume, whereas Europe dominates with over 40% of the total sales.